By Chief China Economist's Office Hong Kong Exchanges and Clearing LimitedSUMMARY

Bond Connect is an arrangement that enables Mainland and overseas investors to trade bonds on the Mainland and Hong Kong bond markets through the connectivity established between the financial infrastructure institutions in the Mainland and Hong Kong. Bond Connect is a major milestone of deepening mutual market access between the Mainland and Hong Kong. As a more efficient market opening channel that runs in parallel to the existing ones, Bond Connect is an innovative and explorative initiative in many ways, one which can attract a broader group of overseas investors to participate in the China Interbank Bond Market and an arrangement that international investors can better adapt to and more familiar with.

The innovations under Bond Connect are manifested in the areas of market admission in pre-trade, price discovery and information communication in trading, and custody and settlement arrangements in post-trade. It effectively connects the Mainland bond market with international practices, at lower access costs and higher market efficiency. On 3 July 2017, the Northbound Trading Link of Bond Connect was officially launched. A trading volume of more than RMB 7 billion was recorded that day. Within three months after launch, foreign holdings of the domestic debt securities increased significantly from RMB 842.5 billion to RMB 1,061.0 billion1, which might be attributable to the launch of Bond Connect. This reflects to some extent the positive impact of Bond Connect on overseas participation in the Mainland bond market.

Bond Connect further opens up the Mainland bond market in a controlled manner, thereby providing new impetus to the market’s international participation, the continued market open-up and reform, as well as to RMB internationalisation. Through Bond Connect, Hong Kong could become a convenient window for overseas investors to gain access to the Mainland bond market. This would further reinforce Hong Kong’s position as an offshore RMB centre, foster the building up of an ecosystem of onshore and offshore RMB products around Bond Connect, and strengthen Hong Kong’s role as an international financial centre and its intermediary function for capital flows into and out of the Mainland.

1.AS A NEW BREAKTHROUGH IN THE OPENING UP OF THE MAINLAND FINANCIAL MARKET, BOND CONNECT HAS SIGNIFICANT IMPLICATIONS IN ATTRACTING INTERNATIONAL CAPITAL TO THE MAINLAND BOND MARKET

Bond Connect is an arrangement that enables Mainland and overseas investors to trade bonds on the Mainland and Hong Kong bond markets through the connectivity established between the institutional financial infrastructure in the Mainland and Hong Kong. On 16 May 2017, the People's Bank of China (PBOC) and the Hong Kong Monetary Authority (HKMA) jointly announced their approval of the establishment of Bond Connect. On 3 July, the Northbound Trading Link of Bond Connect was officially launched2, further opening up the Mainland financial market. With the continuous development of the mutual market access between the Mainland and Hong Kong in recent years and the successive launch of the Shanghai and Shenzhen Stock Connect schemes3 (collectively referred to as the “Stock Connect”), mutual market access is basically achieved between the Mainland and Hong Kong stock markets. As bond market is another key component of the capital market, Bond Connect is considered to be another innovative breakthrough in the opening up of the Mainland financial market in view of the tremendous room for development in the Mainland bond market and the growing international demand for RMB assets.

1.1Tremendous room for development in the Mainland bond market

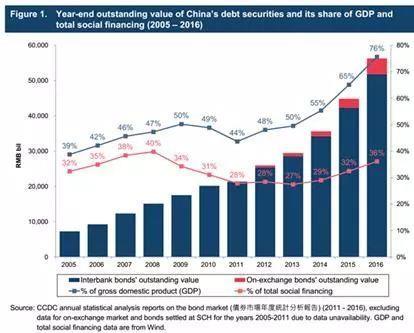

As the Mainland financial market continues to transform, the opening up of the bond market has become a critical force driving the opening up of the Mainland financial market and the internationalisation of the Renminbi (RMB). At the end of March 2017, the Mainland bond market was the world’s third largest after the US and Japan, with a total outstanding value of RMB 66 trillion and with the total outstanding value of corporate credit bonds being Asia’s largest and the world’s second largest4. Nevertheless, foreign participation in the Mainland bond market remains relatively low. If appropriate opening-up measures are adopted to attract more foreign participation in the Mainland bond market, not only will the reform of international balance of payments inflow be facilitated and the ability to reduce fluctuations in the international balance of payments be improved in the short-term, the liquidity of the Mainland bond market will also be enhanced in the medium to long term.

1.2The pace of opening up the Mainland bond market to overseas investors has accelerated in recent years

The Mainland opened up its interbank bond market for the first time to qualified foreign institutions in 2010 and launched the RMB Qualified Foreign Institutional Investor (RQFII) scheme in 2011. Two years later, in 2013, Qualified Foreign Institutional Investors (QFIIs) were allowed to participate in the China Interbank Bond Market (CIBM). In 2015, various initiatives that substantively facilitated overseas investors’ access to the CIBM were implemented. These include: in June 2015, the PBOC allowed overseas RMB clearing banks and participating banks that had entered CIBM to conduct repurchase (repo) transactions in Mainland bonds; in July 2015, the PBOC adopted policies to further facilitate investments on CIBM by overseas central banks and institutions of a similar nature (including foreign central banks or monetary authorities, sovereign wealth funds and international financial institutions), allowing them to expand their investments to cash bonds, bond repos, bond lending, bond forwards, interest rate swaps (IRS), and forward interest rate agreements (FRA), etc.; in February 2016, the PBOC announced new rules that further relaxed the eligibility of foreign institutional investors for entering CIBM, with detailed rules released in May 2016 to expand the scope of eligible foreign institutional investor types and eligible trading instruments, to abolish the investment quota and to simplify the investment procedures. Prior to the launch of Bond Connect, there were 473 overseas investors participating in CIBM, with bond holdings exceeding RMB 800 billion

1.3Bond Connect has positive impact in attracting international capital

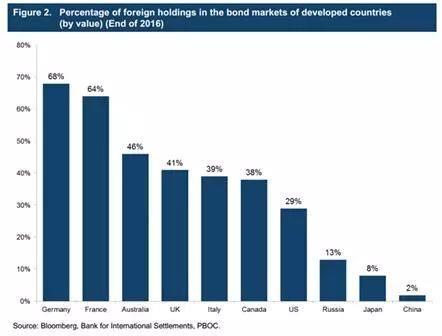

The above measures in exploring the opening up of the Mainland bond market have laid the foundation for the launch of Bond Connect. However, at the end of 2016, foreign holdings in Mainland bonds remained under 2%, which was notably below the average level of opened-up bond markets in developed economies (see Figure 2). The existing access channels of the Mainland bond market mentioned above mainly suit overseas central banks and large institutions that are relatively more familiar with the Mainland bond market and can afford higher operational costs to participate in it. For a large number of small to medium-sized overseas investors, new channels are needed to attract their participation and to address the challenges they encounter when participating in the Mainland bond market. It is against such a background that Bond Connect was launched.

In October 2016, the RMB was officially included in the Special Drawing Right (SDR) currency basket of the International Monetary Fund (IMF) with a weighting of 10.92%. This would bring new participants and capital flow into bond assets denominated in RMB and enhance the global acceptance of the RMB currency as a global investment and reserve currency, thereby boosting international institutional demand for RMB assets in both the public and private sectors. However, the proportion of RMB in official foreign exchange (FX) reserves and FX transactions are currently far below 10.92%. This suggests that the driver for RMB internationalisation in the next stage will come from the proliferation of a diverse suite of investable offshore and onshore RMB-denominated financial assets for international investors. In this context, the opening of the Mainland bond market is a crucial factor. Opening up of the bond market to a larger extent will also foster closer ties between the Mainland regulators and the international market, and promote further internationalisation of participants in the onshore financial infrastructure. Onshore Mainland financial institutions can also develop closer business connections with foreign institutional investors through Bond Connect, paving the way for greater participation by Mainland financial institutions in overseas markets.

2.BOND CONNECT EFFECTIVELY CONNECTS THE MAINLAND BOND MARKET WITH INTERNATIONAL PRACTICES AT LOWER ACCESS COSTS AND HIGHER MARKET EFFICIENCY

Before the launch of Bond Connect, overseas investors can participate in the Mainland bond market through three main channels — QFII scheme, RQFII scheme and foreign institutions’ direct access to CIBM (CIBM scheme) (see section 1.2 above). Compared to these existing channels, Bond Connect is an innovative breakthrough in the “pre-trade”, “trading” and “post-trade” processes. It has addressed expectations and demands of international investors seeking to participate in the Mainland bond market.

2.1Pre-trade: Market admission and parallel channels

Same as the scope of eligible investors trading in the Mainland bond market through existing channels as regulated by the PBOC’s Public Notice No. 3 [2016], overseas investors trading under Bond Connect are mainly central-bank-type institutions and medium- to long-term investors with a focus on asset allocation. This reflects that the Mainland is steadily implementing its strategy to open up the RMB capital and financial accounts and provide new alternative and convenient channels in terms of market admission, filing procedures, eligibility approval and other areas for the entry of long-term capital into the Mainland bond market. While existing channels might satisfy the needs of overseas central banks and large institutional investors to invest in the Mainland bond market, there are certain investors who are interested in investing in the Mainland bond market but are reluctant to bear the high participation cost. That is to say, under Bond Connect, there is no need for overseas investors to have in-depth understanding of the onshore trading and settlement systems of the Mainland bond market and the related Mainland laws and regulations. They only need to use the current trading and settlement practices they are familiar with. Such an arrangement

considerably lowers the entry barriers and costs for overseas investors to participate in the Mainland bond market. Bond Connect is therefore a more user-friendly bond investment channel for overseas investors, as illustrated below.

Firstly, before the launch of Bond Connect, overseas investors mainly accessed CIBM through settlement agents, i.e. as “Type C” participants. In this way, foreign institutions are required to complete the necessary filing and account opening procedures through a domestic CIBM settlement agent for market entry. These procedures, to a certain extent, created obstacles for certain institutional investors to tap into the Mainland bond market. On the contrary, under the more liberalised Bond Connect mechanism, foreign institutions can gain access to the Mainland bond market through a single entry point via offshore infrastructures. Overseas investors do not need to open Mainland settlement and custody accounts and are not required to directly deal with Mainland authorities for market admission, trading qualifications and other related issues. They can make use of their existing accounts in Hong Kong to directly access the Mainland bond market. They are assured at the outset of trading that they can adhere to their familiar international laws and trading practices and at the same time fulfill market admission and filing requirements through offshore financial infrastructures. There is no need for them to get familiarised with the Mainland market practices that differ from their long-established trading and settlement practices.

In operation, the Bond Connect Company Limited (BCCL), established offshore jointly by Hong Kong Exchanges and Clearing Ltd (HKEX) and China Foreign Exchange Trade System (CFETS), provides professional guidance on market access, application review and other market-access preparation support. The time taken to process an admission filing with the PBOC is substantially shortened. In terms of operational procedures, accessing the Mainland’s onshore bond market via Bond Connect aligns more with the trading practices of international investors, particularly for those institutional investors who would like to access the Mainland bond market but are unfamiliar with its rules. Bond Connect essentially enhances the pace of market entry and participation efficiency of these investors in the Mainland bond market.

Secondly, under the current regulatory requirements, overseas investors investing in the Mainland bond market through the QFII, RQFII and CIBM schemes are required to comply with certain requirements upon market entry, including those on fund remittance and lock-up period. They are also required to specify at the outset their planned investment amounts that have to be fulfilled in subsequent transactions (see Table 1). This, at times, may not align with the investment strategies of certain foreign institutions for flexible utilisation of funds. This is also an attribute that has deterred foreign institutions from entering the onshore bond market. Bond Connect, on the contrary, has no such restrictions at market admission, such that overseas institutions face far fewer obstacles at market entry and can directly manage their onshore transactions, allowing greater flexibility in their RMB asset allocation. This will undoubtedly increase the incentive for overseas institutions, particularly the small to medium-sized institutional investors, to participate in the Mainland bond market.

Thirdly, the market access channel of Bond Connect co-exists with the existing QFII, RQFII and CIBM schemes. Overseas investors can now choose among the multiple channels with flexibility. After the launch of Bond Connect, overseas investors are able to choose an investment channel that better suits their strategies. This enables diversified and effective asset allocation and product development in the Mainland’s onshore financial market. Similar adjustments in the choice of investment channels were observed after the launch of Stock Connect. This shows that existing market opening channels are complementary to each other, rather than a replacement or substitution, to serve different investment needs of a diverse investor base. Bond Connect advances the opening up of the Mainland bond market, and helps drive forward RMB internationalisation and the Mainland’s capital account liberalisation.

2.2Trading: price discovery and information efficiency

The Mainland bond market adopted three trading modes: voice trading, click-to-trade and Request-for-Quote (RFQ). As voice trading is done offline, bond trading in the Mainland market could be difficult for overseas institutions to understand in depth. Under Bond Connect, overseas investors can conduct interbank cash bond trading with the Mainland market makers by way of submitting RFQ via offshore platform, after which market makers can provide tradable price quotes for overseas investors to choose and confirm transactions. To overseas institutional investors who are not so familiar with the Mainland bond market, such trading arrangement is simpler and the price and transaction data is more transparent, symmetric and more conducive for price discovery.

Moreover, under the agent bank model, overseas investors cannot directly trade with a Mainland counterpart. They can only entrust agent banks in the Mainland to do trades on their behalf. Under Bond Connect, overseas investors can freely select a market maker for quotes and decide the timing of a transaction via an overseas electronic trading platform using an interface and trading mode they are familiar with. As a result, these overseas investors who invest in the Mainland bond market through Bond Connect do not have significant switching costs during actual operations. To those small to medium-sized overseas institutional investors who are sensitive to transaction costs, this factor is particularly important. At present, Tradeweb is the first overseas electronic trading platform available to investors for Bond Connect. Bloomberg and other electronic platforms are actively progressing on connecting with the Bond Connect platform and will launch their systems once they are ready. The ability of overseas institutions to directly request for price quotes and trade with Mainland institutions without the need to change their own trading practices has enhanced the transparency and efficiency of the entire trading process.

From the perspective of market operation, Bond Connect provides overseas investors with a channel of direct trading alternative to the existing model of agency trading as “Type C” participants. To overseas investors, particularly the institutional investors who are not so familiar with the Mainland market, Bond Connect has, to some extent, reduced agency and communication costs and increased trading efficiency, thereby contributing to the enhancement of market liquidity.

2.3Post-trade: custody and settlement

The Mainland bond market currently adopts a single-level depository system, which is an important arrangement after due consideration following a long period of practical experience to conform to the characteristics of the Mainland bond market. In the offshore market, however, a multi-level depository arrangement with a nominee system has been the long-standing practice. Such difference in practices has created obstacles for overseas institutions to participate in the Mainland bond market. As the multi-level depository arrangement and nominee system in the international bond market have evolved over years to its present form, the business operations of overseas institutional investors have become strongly adapted to it. Should there be any major changes in this operating model, the compliance and back-end operation departments of overseas institutional investors, and the relevant regulators in the local jurisdictions, will face significant adjustment difficulties. This will restrain certain institutional investors from participating in the Mainland bond market.

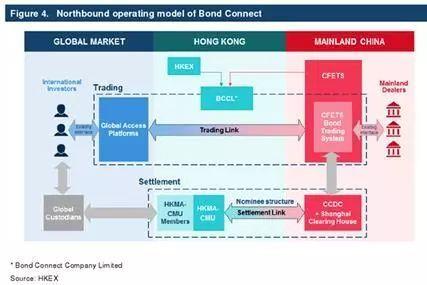

Bond Connect effectively connects the “single-level depository system” as required under the see-through custodian model of the Mainland and the “multi-level depository system” under the nominee model adopted in the international bond market. For the registration, depository, clearing and settlement of bonds for overseas investors, a settlement link is established between CCDC and SCH as the onshore central depository institutions, and the Central Moneymarkets Unit of the HKMA (HKMA-CMU) as the offshore central depository institution. In this way, overseas institutions can observe Mainland market rules while adopting their long-established international practices at the same time, thereby effectively reducing the access costs involved in the operation under different market structures. The arrangement is also conducive to the development of related financial products and business models after the launch of Bond Connect. (See Figure 4 for the operating system set-up of Northbound Trading under Bond Connect.)

In terms of legal framework compatibility, the trading and settlement activities under the Northbound Link of Bond Connect shall comply with the regulations and business rules of the place where these activities take place. Under the nominee holding structure, overseas investors shall exercise their rights over the bond issuers through HKMA-CMU as the nominee holder. If there is a default in bond redemption, HKMA-CMU as the nominee holder of the overseas investor and registered as the bondholder, may exercise the rights of bondholder and take legal actions. Meanwhile, the overseas investor as the beneficial owner of bonds, upon provision of relevant evidence, may also take legal actions in its own name in Mainland China.

3.BOND CONNECT HELPS DRIVE MAINLAND FINANCIAL MARKET OPENING AND DEVELOPMENT OF THE OFFSHORE RMB CENTRE IN HONG KONG

3.1Further opening up the Mainland bond market in a controlled manner

Similar to Stock Connect that has been smoothly operating, Bond Connect has also adopted a closed-loop design ensuring that the market opening brought about by the scheme is under control. In other words, it is an innovative method deployed to further open up the Mainland bond market. Stock Connect is a breakthrough achieving two-way capital flow between the Mainland and Hong Kong stock markets. Compared to the QFII and RQFII schemes, Stock Connect offers more relaxed investor eligibility and more flexible quota controls, and involves lower transaction and conversion costs. After abolishing the aggregate quota in Stock Connect, the closed-loop design reduces the risks caused by substantial capital flow into and out of the Mainland financial market.

For Bond Connect which was launched in July 2017 beginning with Northbound trading, there is also no aggregate quota and the system also operates in a closed-loop structure. By connecting cash bond markets in the Mainland and Hong Kong, the scheme is expected to help funnel international capital into the Mainland bond market, facilitating the internationalisation of the Mainland capital market.

3.2Further strengthening and reinforcing Hong Kong’s status as an offshore RMB centre

Hong Kong has been a global offshore RMB business hub6. The use of RMB is no longer limited to cross-border trade settlement as in the initial stage, but has also extended to a considerable level to the areas of investment, financing, hedging and foreign reserves management. Offshore RMB FX trading volume has also continued to grow7. The sequential launch of Shanghai Connect and Shenzhen Connect, together with the abolition of their aggregate quota, provide new channels for the opening of the Mainland capital market. Bond Connect serves a bigger purpose of complementing Hong Kong’s capability in its bond market development as an international financial centre (IFC). The Southbound Bond Connect will be explored at a later stage, which is expected to attract even more Mainland capital into Hong Kong, bringing greater momentum to Hong Kong’s bond market and its overall financial system.

3.3Building an ecosystem of onshore and offshore Renminbi products associated with Bond Connect

Given the specific characteristics of the Mainland bond markets, the BCCL is expected to perform a prominent role in investor education and market coordination. The launch of Bond Connect and the smooth operation of BCCL would have a profound effect on the Mainland’s onshore and offshore bond markets, in particular, in shaping the onshore and offshore financial markets towards an ecosystem associated with bond asset allocation. As bond markets are dominated by institutional investors, bond trading is closely intertwined with demands for financial derivatives trading and risk management. Bond Connect is expected to bring more international bond investors to Hong Kong to trade offshore debt products on Mainland assets. This could bring impetus to Hong Kong’s bond market and drive demand for professional services in financial derivatives and risk management in RMB, and thereby benefiting the overall industry.

Currently, the Mainland domestic derivatives market offers a variety of tradable products (including forwards, swaps, options and treasury bond futures), with considerable depth and liquidity, to support hedging against RMB-related risks. Lately, the further opening up of the domestic FX market has made it possible for certain qualified overseas investors to directly make use of the domestic derivative products. Concurrently, the Hong Kong OTC market offers a series of RMB products, including RMB FX spots, forwards, swaps and options. Similar exchange-traded products, including RMB currency futures, options and treasury bond futures8, are also available on HKEX. All these products enable overseas participants to better hedge against their exposure in Mainland bond assets and FX risks. Upon the launch of Bond Connect, professional services in Hong Kong that are ancillary to the scheme, such as risk management and innovative RMB-denominated financial instruments, are expected to gain further traction.

3.4Smooth operation drives overseas participation in the primary market of domestic bond issuance

The Northbound Trading Links of Bond Connect was launched on 3 July 2017 with active turnover. A total of 19 participating dealers and 70 overseas institutions executed an aggregate of 142 trades, amounting to RMB 7,048 million, on its debut. By the end of September, 184 overseas institutions have tapped into Mainland bond market via Bond

Connect. Foreign holdings of Mainland domestic bonds also significantly increased from RMB 842.5 billion as of end-June before launch to RMB 1,061.0 billion9 as of end-September. Such an increase may be attributable to the open channel and innovative regime of Bond Connect.

Direct subion of Mainland bond issues by overseas investors was also allowed at the inception of Bond Connect. Five debt financing instruments with an aggregate value of RMB 7 billion were issued by non-financial enterprises on the scheme’s debut. During the first month after launch, 4 financial bonds and 14 commercial papers with a total issue size of RMB 60.68 billion and RMB 15.5 billion respectively were issued to Mainland domestic investors and overseas investors10. On 26 July, the Hungarian Government was the first to issue a three-year Panda Bond of RMB 1 billion11, which was available for subion via Bond Connect. By the end of August 2017, CIBM bond issuers using Bond Connect included state-owned enterprises, local government enterprises and overseas governments, covering the sectors of power, telecommunications, transportation, metals, agriculture and forestry, etc. This shows that Bond Connect is gradually becoming a key channel through which overseas institutions participate in the Mainland primary bond market and has facilitated the diversification of the investor base in the market.

4.CONCLUSION

In conclusion, Bond Connect allows, for the first-time in history, overseas funds to trade onshore Mainland bonds via offshore infrastructure in Hong Kong for trading and settlement. Drawing on the success of Stock Connect, Bond Connect expands the channels through which overseas investors can trade in Mainland onshore bonds, and further opens up the market while retaining the long-established trading and settlement practices in overseas markets. The innovations of Bond Connect are manifested in pre-trade market admission, price discovery and information communication during trading, and post-trade custody and settlement. This effectively connects international practices and the Mainland bond market at lower access costs and higher market efficiency.

As a major IFC in the region, Hong Kong provides Bond Connect with a trading and settlement platform that conforms to international practices, bridging the Mainland and global capital markets. More entities would be attracted to participate in the Hong Kong financial market, bringing in more capital and widening the range of RMB financial products in the city. All these would facilitate the development of Hong Kong as a RMB asset allocation centre and solidify Hong Kong’s status as an offshore RMB centre.

In the long term, Bond Connect would significantly improve the efficiency of cross-border investment capital flow and enhance the internationalisation of the Mainland market. The implementation of Bond Connect is expected to foster the further development of financial products and services associated with onshore RMB bonds, and contribute to the development of a more diversified investor base and a more open bond market for the Mainland.

文章来源:香港交易所官方网站2017年11月15日(本文仅代表作者观点)